Recently, Paul Rosenberg published a piece called: ““Stimulus for Dummies” — A Public Service Instruction Guide.” at Open Left. It had previously appeared in Random Lengths News, where he is Senior Editor, I appreciate Paul’s attempt to try to explain the stimulus to some imaginary skeptic, though I’m not altogether taken with calling the skeptic “Dummy.” Nevertheless, on reading his piece, I thought it was a little bit off the mark and failed to clearly explain some very fundamental ideas related to Government spending and the stimulus that I think “Dummy,” as well as well as most progressives who may have found themselves agreeing with Paul’s piece, really need to know. So here goes my attempt to explain these fundamentals cast in terms of comments by a fictional “Stimulus for Smarties,” replying to Paul’s imaginary dialog between “Dummy” and ‘Stimulus for Dummies.” To cut down on the length of this I’ll quote Paul in part, and also summarize some of what “Stimulus for Dummies” has to say.

Dummy Asks: What’s the difference between deficit and the debt? And why do they matter?

Stimulus For Dummies Responds: The deficit is the annual shortfall between government income and expenditures. The debt is the total of all past deficits, offset by past surpluses (the last of which occurred under President Clinton.) By themselves, neither the deficit nor the debt are good nor bad, it depends on the context-just as taking out a loan to buy house or a car isn’t the same as taking out a loan to go to Vegas.

What’s more significant is the debt-to-GDP ratio, the debt divided by the size of the economy, which should go up in the case of an obvious need as it did for World War II, for example. The debt-to-GDP ratio should stabilize or go down when things return to normal. There is nothing wrong when the government runs a deficit, but the debt-to-GDP ratio goes down. Long-term growth will more than compensate for the short-term shortfall. What’s problematic is when debt-to-GDP ratio goes up and there’s no obvious need for it to do so, as happened under conservative Republican presidents Ronald Reagan, George H.W. Bush and George W. Bush.

Stimulus for Smarties Comments: Actually, neither the deficit, nor the debt, nor the debt-to-GDP ratio are significant in themselves, for nations whose deficits and debts are incurred in their own fiat currency. This is not because taking out a loan to buy a house or a car is different from taking one out to go to Las Vegas, though it is true that spending to create greater value will create real wealth and be better for the real economy of a nation over time, than spending wastefully. But rather, it is because nations whose deficits and debts are incurred in their own fiat currency do not fund their expenditures by borrowing money. Instead, they spend by simply issuing credits to private or public sector accounts or by printing money. So, the size of their deficits or their national debt, or the ratio of that debt to their GDP has no necessary implications for their continued ability to spend, or if they wish to reduce their deficits, national debts, or debt-to-GDP ratios, in the future. In short, it is wholly inappropriate to worry about any of these things, or to create “rules of thumb” for public policy around them, or to view them as triggers for Government economic policy in any way.

These measures were relevant to economic policy when the United States and other nations were on the gold standard, and they may still be relevant for nations like Greece and other nations who have foolishly given up their sovereign authority over their own currency to the European Union, or perhaps to the IMF, or some other International organization. But for most nations today, who retain monopoly control over their own currency and their ability to issue it, the health of their economies is a function of things like levels of employment, quality of health care, life expectancy, infant mortality, equitable distribution of valued economic outputs, happiness at work, life satisfaction, environmental quality, freedom from want, and other things that are real and concrete to the human beings the economy serves. It does not depend on other people’s currency.

Dummy Says: Families across America are cutting back on their spending. Government should cut back, too!

Stimulus For Dummies Responds: When times get hard, people cut back on spending. While this makes sense for the individual, it’s bad for the economy because everyone cutting back on spending means less income for everyone else, creating a vicious circle that drives the economy deeper into recession. Government spending can break this vicious circle by pumping money into the economy when everyone else is pulling money out. But it has to be enough spending to make a difference, just as it takes enough effort to push a car uphill and over the top. Otherwise, the car will just run back downhill again. Not spending enough in the first place or cutting back prematurely will undercut the effectiveness of spending to get out of a recession. This happened when Franklin D. Roosevelt prematurely cut back on spending in 1937, causing a recession that lasted two years. And, it happened repeatedly in the 1990s in Japan, giving rise to what’s known as the “lost decade.”

Stimulus for Smarties Comments: This is right as far as it goes; but it misses a very fundamental point. The Government is not like you or me, or our households, or our enterprises public or private, or even like American State Governments in at least one very important way. And that is that it has the authority to create money and make expenditures at will. Though it collects money through taxation, and also borrows money from non-Governmental agents including foreign Governments, its authority to spend is in no way operationally limited by either what it raises through taxation or what it raises through borrowing. Its only limitations in its ability to spend are self-imposed ones such as Congressional limits on the size of the national debt. So when hard times come, and it is rational for everyone else, states, businesses, non-profits, families, and individuals to cut back on what they spend and “tighten their belts,” it is not rational, and, in fact, it is absolutely the wrong thing to do, for Government to do the same. Instead what Government ought to do is to pick up the slack for declining demand from everyone else. It ought to spend and to invest in the economy, especially in those areas of value which private economic activity has neglected even at its height. It ought to invest in order to create a new job for every lost job, and in sufficient volume that renewed economic activity and full employment is the result of its efforts. Right now our Government isn’t doing that. And it isn’t doing it because it’s managing the economy based on false beliefs about deficits, debts, and debts-to-GDP ratios that lost their relevance when the United States ended the convertibility of US Dollars to Gold in 1971, and adopted a fiat money system in place of the previous commodity money system ultimately based on Gold.

Dummy Says:The Stimulus hasn’t created any jobs!

Stimulus For Dummies Responds: You’ve heard this a lot from Republican politicians when they’re in the District of Columbia. They said this when almost all of them voted against it originally and they’ve said it repeatedly since then. But either behind the scenes or out in public when they’re in their home districts, they sing a very different tune. . . . And Paul then quotes news accounts about the large number of Republicans in both the Senate and the House who have both “railed” against the stimulus legislation and actively sought stimulus funds for their constituents while claiming to those same constituents that the funds would create or save jobs in direct contradiction to their earlier and continuing claims that “the stimulus hasn’t worked.” Paul then quotes Dean Baker and says:

Finally, “About one-third of the stimulus was tax cuts, not spending,” said economist Dean Baker, co-director of the The Center for Economic and Policy Research. Republicans have always touted tax cuts for stimulating the economy and creating jobs. But most economists agree that tax cuts do less to stimulate the economy than government spending because tax cuts more often go to paying down debt, rather than generating new economic activity. Nonetheless, the stimulus has been effective enough to dramatically reverse the mounting job losses that preceded its passage:”

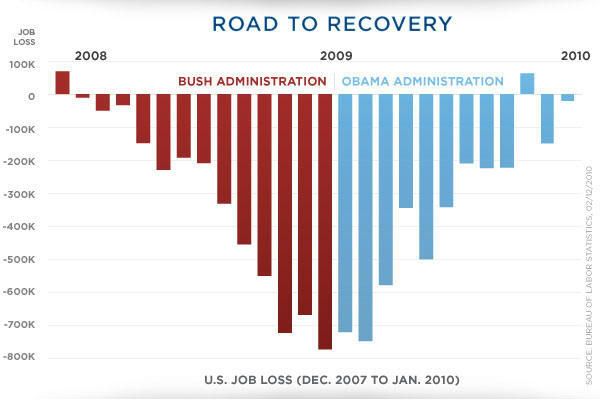

And then Paul follows this with a graphic showing job losses steadily increasing during the Bush Administration and then steadily decreasing at approximately the same rate after passage of the Stimulus by the Obama Administration.

{kind=link}

Stimulus for Smarties Comments: Well it’s nice to know that many Republicans in Congress are hypocrites, and that even while condemning the stimulus legislation they also make public statements showing that they believe it will do some good for many of their constituents. It’s also nice to know that most economists believe that the public expenditure portion of the stimulus package is more effective than the tax cut portion. But neither of these comments answers what the “Dummy Says.” To answer that, one has to make the case that the stimulus did create jobs.

That case is not made by Paul’s graphic showing that the level of job losses has dropped pretty consistently since the stimulus was passed, because: correlation is not causation; a decline in the number of jobs lost each month is not prima facie proof that any new jobs were created; and also because it is possible that both the decline in jobs lost, and any new jobs that may have been gained were due to natural tendencies for the economy to recover and not Government intervention. However, there is plenty of evidence that the stimulus did both save and create plenty of jobs, and Paul Rosenberg should have cited that evidence in a direct reply to “Dummy” instead of playing on Republican hypocrisy (demonstrating that Republicans are insincere bad boys) and the views of most economists (appealing to authority) that Government expenditures are more stimulative than tax cuts. In brief:

Just look at the outside evaluations of the stimulus. Perhaps the best-known economic research firms are IHS Global Insight, Macroeconomic Advisers and Moody’s Economy.com. They all estimate that the bill has added 1.6 million to 1.8 million jobs so far and that its ultimate impact will be roughly 2.5 million jobs. The Congressional Budget Office, an independent agency, considers these estimates to be conservative.

Dummy Says: Democrats say the stimulus has “saved or created” more than a million jobs. What’s this mumbo-jumbo about “saving jobs”?

Stimulus For Dummies Responds: New job creation through spending was only a small part of the stimulus plan.

“The infrastructure part of the stimulus was relatively small. It was about 13 percent,” Baker told Random Lengths. “Most of the spending went to support state and local governments so they wouldn’t have to make cutbacks and for unemployment insurance.

Still, that support for state and local governments wasn’t enough and will do even less as stimulus funds dry up. These job losses will offset the job-creating impact of the stimulus. . . .

And Paul goes on by citing various reports and news accounts presenting facts supporting the idea that States and local Governments are facing severe budget cuts and impending job losses as the stimulus dries up later this year. And he continues with this:

What’s needed now is much more stimulus funding to keep states and cities afloat to prevent massive job cuts in the next two years, but no one in Washington seems focused on this. . . .

Stimulus for Smarties Comments: Again this is all interesting material, that I’m sure “Dummy” needs to know, but it avoids directly answering the question of whether the stimulus has saved jobs that otherwise would have been lost. The studies I cited earlier provide evidence that large numbers of jobs were saved by the stimulus, This is the direct answer to “Dummy,” and the first thing she/he needs to know.

Then the point can and should be made that the stimulus was not large enough, and that what’s needed now is a much more extensive stimulus that would really end the recession. In making this case, however, the point, not made by Paul Rosenberg, but made by me earlier, that spending by the US Government is not operationally limited by having to raise funds either through increased taxes or by further borrowing, and that the Obama Administration can, if it wishes, add a $One Trillion further stimulus to its present efforts without straining its ability to fund many other expensive programs is overwhelmingly important, because it leads to the question, “why in hell are the Administration and the Congress tolerating 10% unemployment when, collectively, they have all the capability they need to create full employment, if they would only use it?”

Dummy Says: The Stimulus is driving the government to bankruptcy!

Stimulus For Dummies Responds: First, it’s virtually impossible for the government to go bankrupt. The post-World War II debt-to-GDP was 115 percent — much higher than today — and we cut it rapidly in the following few years. Japan’s current debt-to-GDP ratio is almost 200 percent and no one is panicking over it. Second, the vast majority of our current deficit is the result of Bush-era policies, including tax cuts and military spending. This will remain so for the next decade and more. . .

Third, almost every President since World War II has reduced the debt-to-GDP ratio, except for so-called “conservative Republicans,” Reagan and the two Bushes . . .

Stimulus for Smarties Comments: The problem with this answer to “Dummy,” is that it tacitly grants the idea that the deficit-to-GDP ratio is important and that if it gets high enough it is something we have to be concerned about. In saying that it is “virtually impossible” for the US Government to go bankrupt; it is granting that bankruptcy is a possibility if only deficits get high enough. In other words, it tells “Dummy,” look, I agree with you that bankruptcy is a possibility, but as a practical matter it won’t happen, so you don’t have to worry about it, and also any bankruptcy won’t be due to Obama’s stimulus, but will be due much more to Bush’s tax cuts, the Wars, and the long-term effects of the recession Obama is fighting.” This is a pretty good answer to “Dummy” for some, perhaps; but it is not the right answer.

The right answer is that barring the Government’s and the Congress’s misunderstanding of how money is created in fiat money systems, followed by a declaration by them that the US is defaulting on its debts, there can be no such default/bankruptcy, simply because the US Government has no limits on the money it can generate to meet its debt obligations. It is sovereign with respect to its fiat currency, and it owes no debts to anyone in any other currency. So whenever a demand for repayment is made by any creditor of the United States, that creditor can be instantly repaid by the Federal Government, barring any self-imposed constraints originating in the Congress or in the Administration. So, ‘Dummy’s” concerns over the possibility of bankruptcy are entirely unwarranted, and they derive solely from “Dummy’s” mistaken assumption that the US must raise money either by taxing or borrowing in order to pay its debts. To get “Dummy” thinking straight he/she has to be persuaded to give up that false assumption, and come to an understanding that the Government (including the combination of the legislative and executive branches), has unlimited authority to spend either to pay its debts, or to make whatever investments in the economy and American society, it thinks are useful and warranted.

Dummy says: The stimulus has made us dependent on foreign lenders like China!

Stimulus For Dummies Responds: Baker said it best. “We don’t need China to lend us money and in fact would be better off if they didn’t,” Baker told Random Lengths. “China’s lending is how it ‘manipulates’ its currency by keeping it low against the dollar. If it lent us less money, the yuan would rise and our trade deficit with China would shrink.”

Stimulus for Smarties Comments: Baker is right that “we don’t need China to lend us money. . . .” But, even though the fact that China manipulates its currency, in part, by lending to us, is very interesting for “Dummy” to know, it is not the reason why “we don’t need China to lend us money.”

That reason, instead, is simply, and, once again, what Paul Rosenberg won’t explain to “Dummy:” namely, that China need not lend us money because our ability to spend is not in any way limited by the money we raise through borrowing and through taxation. The fact is that the Government borrows money from others including China to maintain our domestic interest rates at a greater than zero level. And it taxes us not for the money produced through taxation, but because our need to pay taxes creates a demand for its monopoly currency. But to get the money it spends, it doesn’t either borrow or tax. It just issues the money by crediting the bank accounts of those it wants to pay, by sending them checks, or theoretically by sending them newly printed greenbacks, though it never does that these days.

There’s much in Paul Rosenberg’s dialogue with “Dummy” which is interesting and important. However, where it misses the mark, is that again and again, in reply to “Dummy’s” assertions, he fails to make the fundamental point that the United States has a fiat currency and the Government is the monopolist of this currency and, that, neglecting self-imposed constraints, it has unlimited authority to create and spend US Dollars. So, he doesn’t provide bottom line explanations to “Dummy” about 1) why deficit numbers, including deficit-to-GDP ratios don’t matter as standards for evaluating Government policy, 2) why Government should increase expenditures rather than cut back in hard times; 3) why the Government can afford and should enact a massive additional stimulus to end the Great Recession; 4) why the Obama Administration’s stimulus is not bringing the Government to the point of bankruptcy; and 5) why the United States is in no way dependent on China’s continuing to buy Government securities. For “Dummy” to really understand why his views on the stimulus have no basis in reality, Paul needs to go beyond the responses he offered to provide deeper explanations recognizing the actual process by which Government expenditures occur in nations with a fiat monetary system, and the influence of this process on the issues “Dummy” raises.

In a lengthy exchange with Paul, selise pointed out that the US could not be forced into bankruptcy because of the Government’s control over its currency, and she pointed out, further, that understanding this was “absolutely key to breaking the current frame and advancing our understanding of the economic policy space we do have — and not confusing it with today’s political policy space.” Paul replied by saying:

People can only assimilate so much. While it’s certainly true that bankruptcy can’t be forced on a sovereign nation with its own currency, that’s not the fundamental reason why all this debt panic is a load of malarky. The explanations I’m providing are ones that are both sufficient for refuting the avalanche of malarky and are readily graspable.

I have to say I found this both very offensive and also somewhat incoherent. It’s offensive because Paul puts himself in the position of the authority qualified to judge what “Dummy” can “assimilate” and what he or she can’t, and therefore, conveniently, relieves himself of the responsibility of trying to explain clearly why the United States cannot go bankrupt without making a foolish political choice to do so. It’s somewhat incoherent, because Paul asserts that the impossibility of the US going bankrupt is “. . . not the fundamental reason why all this debt panic is a load of malarky.” But, isn’t it? What if we were back on the gold standard and did not have a fiat monetary system? Is it then so clear that debt panic would be “a load of malarky”? I don’t think so. All we have to do to refute this view is to look at recent examples of countries that lost control of their currency to external authorities, and ran into debt difficulties: Zimbabwe, Argentina (which had to default and regain control of its fiat money system before it could get its economy under control), and now, Greece, and perhaps in the very near future: Portugal, Ireland, Spain, and even Italy (all of which have given up control of their currency to the EU). The point is that the fundamental reason why a nation may have to fear bankruptcy and be concerned about such things as deficits, national debts, and deficit-to-GDP ratios, is that it has arranged things so that its currency is convertible to something not entirely under its control, such as Gold, or the Euro, or other foreign currencies. Paul says that: “The explanations I’m providing are ones that are both sufficient for refuting the avalanche of malarky and are readily graspable.” But I think I’ve shown above that they are not sufficient, and, I think, further, that Paul’s judgment about what is “readily graspable” by “Dummy” and what is not, is probably relative to what Paul himself “grasps.”

So, the question arises does Paul “grasp” what it means to have a fiat monetary system? Does he “grasp” the difference between economies that have such a system and those that do not? Just after the passage quoted just above Paul says:

. . . . hyperinflation does remain a very real possibility, given what’s already happening with the rating agencies driving up the cost of borrowing for cities and states that actually could do some of that to ease their situations. I’m not talking about this happening to US currency tomorrow. But it’s certainly a much more palpable possibility than anyone could have imagined just two years ago.

But there is no comparison of the situations of the states and cities with the situation of the US Government, just because the Government controls the currency and the states and cities incur debts in that currency without having the authority to issue it at will. States and cities can only spend the money they raise from taxing and borrowing, while the US Government doesn’t even tax and borrow in order to raise money for its expenditures. Does Paul Rosenberg “grasp” these fundamentals of fiscal reality? The remark I quoted just above suggests that he does not. And his notion that hyper-inflation in US currency is more of a possibility now than it was two years ago is a purely subjective assertion based neither on cogent economic theory, nor on any empirical evidence. It is every bit as far-fetched as the frequent claims of “the deficit mongers.” And it is an assertion that suggests that Paul needs to begin serious research not only into Galbraith’s work, but also into Randall Wray’s, Bill Mitchell’s, Warren Mosler’s and other writings in Modern Monetary Theory, so that he can begin to “grasp” what it means to have a modern fiat monetary system.

(Thanks to Lambert for calling Paul Rosenberg’s blog to my attention and suggesting I offer a reply)

(Also posted at firedoglake.com and Correntewire.com where there may be more comments)